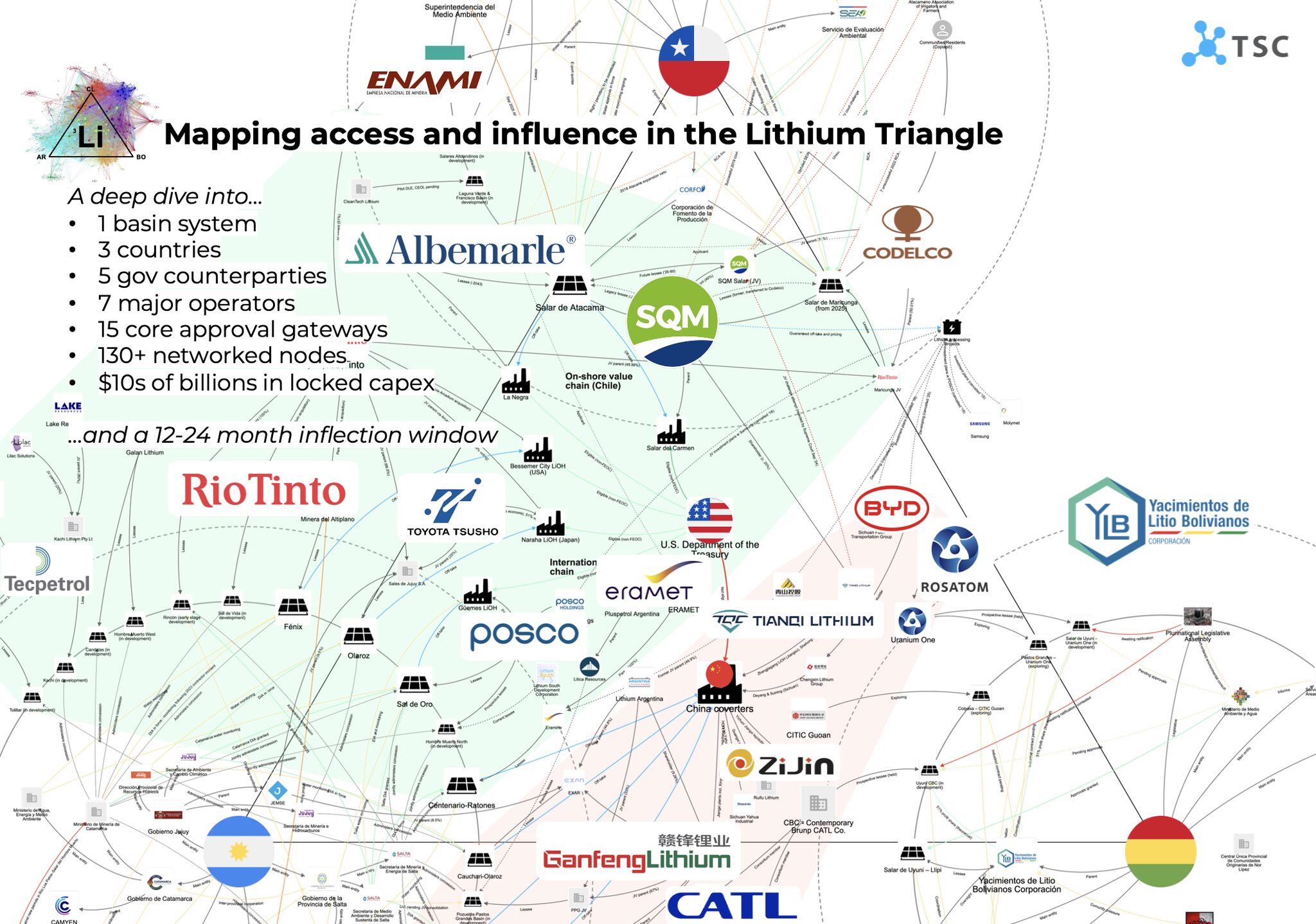

The Lithium Triangle represents the world’s largest untapped lithium prize, with 50%+ of global resources but only ~28% of output.

That growing supply is currently in the hands of just 7 major operators: SQM, Albemarle Corporation and Rio Tinto in Chile + Rio, Eramet, POSCO HOLDINGS, Ganfeng Lithium LATAM and Zijin Mining Group in Argentina.

We mapped the stakeholders networks shaping the future of the clean energy transition. The space is at an inflection point:

1. Lithium is driving serious Capex as the upstream consolidates.

✅ Rio Tinto has spent more than $10bn in the last three years, Ganfeng -more than $3bn, Albemarle - more than $2bn.

✅ Exploration continues to move, with dozens of projects in the pipeline.

✅ Recovering but still volatile prices will set payback periods & exploration appetite.

2. Geopolitical tensions are bifurcating the market.

✅ The US treasury’s foreign entity of concern (FEOC) rules go live in 25, splitting the value chain in two.

✅ New converter capacity is coming onstream in the EU and NA, weakening the current Chinese bottleneck.

✅ Upstream consolidation shifts deal leverage in favour of miners, supporting prices and creating an ‘eligibility premium’ for clean sinks.

3. The Triangle is a poster child for above ground risk variables.

✅ Water and consent increasingly exist as a cost of capital.

✅ Local approvals - complex, sensitive, and increasingly collective, shifting toward basin-wide rather than project-specific assessments.

✅ Brazil + Peru are learning the lessons. Their hard-rock projects may turn the Triangle into a Pentagon.

Over the next 12-24 months, competitive advantage will come down to world-class stakeholder management, but operators have underinvested in their toolbox.

Download an exclusive high-res version that includes the >130 networked nodes and ‘soft’ (but existential) variables we are tracking.